How Much Money Do You Need to Retire?

How much money do you need to have saved up before you can retire? This is an often asked question that you generally receive unsatisfactory answers to. I believe this is because the question is often answered by those with a vested interest in you having a LOT of money invested with them, and so they seem to err on the high side. The problem here is that if the answer seems unfeasibly high, then you are likely to not even try. The true answer to how much money you need to retire on, can only really be answered by yourself, as it does depend on what sort of lifestyle you are accustomed to, and what sort of lifestyle you want in retirement. However, chances are, that you can retire on less than many pension advisers will lead you to believe. Remember, when you retire you should be mortgage free and child free, both considerable expenses that you have had in the past that you now no longer have.

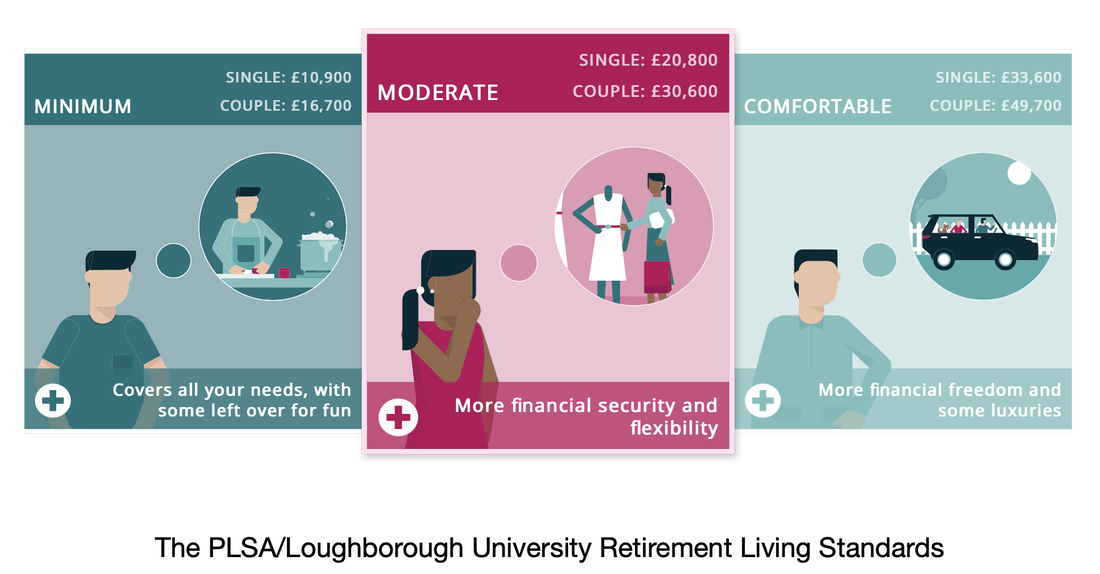

One resource that may help is The Retirement Living Standards based on independent research by Loughborough University. Again, remember that the figures they have produced are generic and your circumstances may vary considerably. However, it does start to give you some ballpark figures to be working with. The amount of money required for either single people or couples to retire on, with minimum, moderate or comfortable lifestyles is shown below. Just remember, if you have not been living at the 'comfortable' end of the scale for most of your life, you probably don't need to be looking at that level of income for your retirement!

One resource that may help is The Retirement Living Standards based on independent research by Loughborough University. Again, remember that the figures they have produced are generic and your circumstances may vary considerably. However, it does start to give you some ballpark figures to be working with. The amount of money required for either single people or couples to retire on, with minimum, moderate or comfortable lifestyles is shown below. Just remember, if you have not been living at the 'comfortable' end of the scale for most of your life, you probably don't need to be looking at that level of income for your retirement!

To calculate how much you need to retire on you therefore need to calculate your living expenses, remembering to include general house upkeep, such as decorating, holidays and gifts as well as everything spent on a monthly basis. Looking at your bank and credit card statements will probably help with this task. To help get you thinking about this I have put together a handy list of possible expenses here - Monthly Expenses

You may be surprised and find that actually you could live on less than you realised each year. Remember you don’t have any mortgage or child costs and you won’t be putting large sums into pension schemes anymore. Let's say that you believe that £2000 per month would be enough (for some people it may be less or more), this would mean an annual income of £24,000 would be sufficient for retirement. Now what if you continued to earn a little money via a part time job? Maybe just £4000 a year? Then your pension pot (and other investments) needs to produce an income of £20,000 per year.

So where is this £20,000 per year going to come from? Well the bulk is likely to come from your pension if you have contributed enough. But you might also have other money invested in ISAs or other savings/investment vehicles.

Let's assume that most of your money is in a pension pot, probably a company pension scheme or a SIPP (Self Invested Personal Pension). Currently you can expect to earn around 4% (Natural Yield*) from a pension pot, and knowing this can help you plan backwards and answer the question 'how much money do I need to retire?' To do this you perform the simple calculation of multiplying the annual income you will need by 25.Therefore if you need your investments to provide you with £20,000 income each year, you need an investment pot of £500,000. (20,000 x 25)

*The theory behind the natural yield approach to investing has been around for generations. Under natural yield rather than selling your investments to fund retirement spending, you simply live off the income these investments produce. This could be dividends if you’re invested in stocks and shares, or interest on bonds or cash. This means that the underlying capital isn't touched and in theory, the underlying assets could continue to grow.

You may be surprised and find that actually you could live on less than you realised each year. Remember you don’t have any mortgage or child costs and you won’t be putting large sums into pension schemes anymore. Let's say that you believe that £2000 per month would be enough (for some people it may be less or more), this would mean an annual income of £24,000 would be sufficient for retirement. Now what if you continued to earn a little money via a part time job? Maybe just £4000 a year? Then your pension pot (and other investments) needs to produce an income of £20,000 per year.

So where is this £20,000 per year going to come from? Well the bulk is likely to come from your pension if you have contributed enough. But you might also have other money invested in ISAs or other savings/investment vehicles.

Let's assume that most of your money is in a pension pot, probably a company pension scheme or a SIPP (Self Invested Personal Pension). Currently you can expect to earn around 4% (Natural Yield*) from a pension pot, and knowing this can help you plan backwards and answer the question 'how much money do I need to retire?' To do this you perform the simple calculation of multiplying the annual income you will need by 25.Therefore if you need your investments to provide you with £20,000 income each year, you need an investment pot of £500,000. (20,000 x 25)

*The theory behind the natural yield approach to investing has been around for generations. Under natural yield rather than selling your investments to fund retirement spending, you simply live off the income these investments produce. This could be dividends if you’re invested in stocks and shares, or interest on bonds or cash. This means that the underlying capital isn't touched and in theory, the underlying assets could continue to grow.