It’s a good idea to have goals I retired early, about 4 years ago now. It wasn’t really really early, and I’m not sure if you could say I followed the principles of FIRE (Financial Independence, Retire Early), but I had always wanted to stop working by the time I had reached the age of 55, and so I did. Because I had given myself the deadline of 55 years young for retiring, I guess that focused my mind a little during my working life. The state pension isn’t available to me until I am 67 years old, and even then, it’s not really enough for me to have the sort of lifestyle that I want. So to achieve my goal I would need to be able to fund myself from 55 to 67 years old and then further supplement the state pension from 67 onwards. Throughout my life, I never felt that I was doing without, or living especially frugal, but having my goal probably helped me to make some ‘better’ financial decisions. Having goals can do that for you. It’s a good idea to have goals for all sorts of things in life and goals around finance are particularly important as money really CAN make you happy, despite what some might have you believe. I should have tracked my investments closer In my late 20s I started a pension scheme, initially a personal one and then a company one. I also started a stocks and shares ISA (it was called a PEP then, but essentially the same thing). An ISA is a U.K. product and it stands for Individual Savings Account. However, there are a number of different varieties of ISA and the stocks and shares ISA enables you to invest up to £20,000 per year in the stock market and all gains and income are completely tax free. I didn’t know much about pensions or ISAs at the time and I just invested regularly in the default funds. When I say regularly, I mean monthly, either through work or direct debit. I hadn’t thought about the concept of ‘compound interest’ or carried out any forecasting to see how much I should put away each month to achieve my goals; I just put away small amounts that I could afford at the time and increased them as I could afford more. It felt like a strategy that made sense if I wanted to be able to accumulate wealth and retire early. Every few years I would have a look at what I had accumulated in my investments and although I wasn’t looking at total net worth, I could see that accumulated wealth was increasing over the years. In hindsight I should have tracked my investments closer, tracked net worth over time and monitored progress towards my goal a little better. Putting money into my pension and ISA was a habit I then worked for around 30 years, focussing on my career and family, and didn’t think much about my investments. Putting money into my pension and ISA was a habit. I put in what I could afford and when my company offered to match a higher pension contribution it seemed like a good idea, and so I increased my contribution to the maximum they would match. Here’s a tip; check your company pension scheme and if they will match your contribution at a higher level than you are currently contributing at, then this is free money you should be taking. Decided to consolidate a number of company pensions In my late 40s and early 50s I started thinking about my retirement goal of 55 a little more seriously. I started to focus on the value of my investments and how realistic my goal to retire early was going to be. I decided to consolidate a number of company pensions that were spread across a number of pension providers. I checked first that I could do this without penalty and then moved them all to Hargreaves Lansdown where I then had complete control over what they were invested in. This also gave me greater visibility and understanding of how much I had and helped me to start thinking about what I needed to do, to enable me to reach my retirement goal. I needed my funds to produce an income Previously, all of my investments, both in my pension and my stocks and shares ISA were in the default accumulation funds. When you are looking to grow your investment, an accumulation fund is fine. This type of fund will automatically reinvest any dividends or interest back into the fund, and this is what helps it grow and gives you the compounding effect over time. However, I needed my funds to produce an income for me during retirement, and so I started to move my investments into income funds. With income funds, any money the fund produces through dividends or interest is paid out as income. Increased the level of diversification I also wanted to reduce any potential volatility within my investments as I approached retirement and so I increased the level of diversification within my fund holding. This meant that in practice I moved from holding 2 or 3 funds to closer to 25 funds split across asset types (shares and bonds) and across geographies. I made all these changes over a number of years; I don’t like to make large scale changes in one go, I make lots of small changes over a long period of time and check that everything is working as planned before taking the next step. Diversification reduces volatility of your investments because if one asset type or geographic area isn’t doing well, then another asset type or area may be doing better, which balances things out somewhat. Always been tempted by property Also as a part of my diversification I started to look at other types of investment. I had always been tempted by property but had never really found the time to pursue buy-to-let properties whilst working. I was still quite hesitant about buy-to-let when I happened to come across a new company called Property Partner. With Property Partner you can buy shares of a property along with other investors and then receive your portion of the rental income each month. After 5 years there is a vote to decide on whether or not to sell the property or keep it for another 5 year term. There is also a secondary market if you need to sell your shares earlier than the 5 year term. From an investors point of view, owning property through Property Partner is a much easier option compared to owning your own buy-to-let property, as it allows you to diversify across a wide range of properties without the worry of property management, as this is all taken care of by Property Partner. It hasn’t been all plain sailing however, and over the last few years, returns have not been as great as expected. However, the company has now been bought by a U.S. mortgage company called Better which has already resulted in some improvements such as lower fees. This along with the post covid recovery could see investor returns improving over the next few years. Currently the rental yields I am receiving are around 3% - 4%, but with the few properties that have gone through the full five year cycle I have made just under 14% return as the bulk of the profit has been through the increase in property value between purchase and sale, rather than through rental yield. Continue to look for new opportunities Recently I have also started to look at a newer company called Proptee. This works in a similar fashion to Property Partner, but uses the power of NFTs (Non-Fungible Tokens) that are associated with real rental properties. It’s an interesting concept that lets you benefit from rental yield and growth in property value, but again with none of the management issues you may have with traditional buy-to-let. As this is a newer start up company built on a newer technology, there is probably a greater risk associated with investing through Proptee than through Property Partner. However, it highlights that as newer technologies develop, so do the opportunities for investors. I continue to look for new opportunities to invest in, but always start cautiously and carry out my own due diligence. Generating un-taxed passive income Soon after my 55th birthday I handed in my notice at work and ‘retired’. In the U.K. you are allowed to withdraw 25% of your pension fund without paying any tax and so this is what I did. This enabled me to buy a car to replace the company car that had to be returned, and the rest went straight back into investments. It couldn’t go straight into my stocks and shares ISA as it exceeded my annual allowance (£20,000), but it was invested in general investment accounts, and over the next few years was gradually moved in to my stocks and shares ISA, invested in funds generating un-taxed passive income. Following a natural yield approach My remaining pension went in to a drawdown account as I believe that the value you get from an annuity is very poor. I’m following a natural yield approach both with my pension and my stocks and shares ISA, which means that I only draw off the income that is produced though dividends or interest and the capital is left untouched. Hopefully in this way, my investments will last throughout my retirement, maybe growing slightly in value and continuing to produce enough passive income for me to have the lifestyle I want. Personal finance is just that; personal This is my story, which I am sure is very different from your story. Personal finance is just that; personal. There isn’t one way that is the right way, just a set of general guiding principles. I didn’t start to gain a real interest in finance until quite late in life. Up until that point, I stumbled along and followed my own gut feelings of what felt right to me. It didn’t work out too bad and I achieved my goal of retiring by 55. But I am sure I could have done things better, invested more, invested smarter and retired with greater wealth than I now have. Please remember, what I have written is not investment advice. But if it makes you stop and think, or if it gives you a new way of looking at things, then I have done my job.

0 Comments

I retired three years ago when I was 55 years young. My plan was to always retire early, for no particular reason apart from the fact that I felt there was more to life than just work, and I wanted to have a good long retirement in which to enjoy it.

I remember when I set up my first personal pension, back in the days before you could do these things yourself on the computer, a pension advisor from Barclays came round and one of the questions he asked was ‘when do you want to retire?’. I told him 55 as that seemed like as good an age as any, and then from that point on, this became my goal. In hindsight I feel that I was actually quite late setting up my pension and thinking about retirement. In an ideal world I should have done this earlier, but I was unsure what I wanted to do with my life, was late going to university, spent four years as an undergraduate and then drifted into post graduate research. I was 27 years old when the man from Barclays asked me what age I wanted to retire, and it was only then that I started contributing to a personal pension plan. I was paying in £30 a month which was around 3.5% of my annual salary as a university Research Associate. I’m not sure what made me decide to start a pension, but it was the start of a life long habit that paid off later in life. I guess the important point here is that you don’t have to start contributing to a pension particularly early in life and you don’t have to contribute a lot to start off with. You probably don’t want to leave it much later than I did, but starting is the key thing. Once you start, it becomes a habit, and the money that goes into your pension is never really missed if it never actually reaches your bank account in the first place. After my research post I got a ‘proper’ job in sales and then had the opportunity to join my company pension scheme. I stopped contributing to my personal pension and instead contributed to the new work pension. I don’t recall much about the details of this pension, but believe I paid a nominal percentage of my income and the company also contributed a small amount. In those days I was less interested in the detail, and anyway, everything was done via letter and access to the detail was not really as easy as it is today. I worked for this company for around nine years and my average salary during that time was probably around £20,000 (starting around £12,000 and rising as I progressed in my career to about £30,000). The total contribution to this pension per year was probably in the region of 8% (3% from me and 5% from my employer), and so over the nine years I was working for them, I would guess that the total contributions to my pension were around £15,000, of which just over £5,000 were taken from my salary. Bear with me, there is a point to all this. After moving to a new company, this pension was frozen and I filed away the details. However, it was still ‘doing its thing’ in the background, growing slowly at first and then more and more over time as growth was applied to the original investments and all previous year’s growth (the compounding effect). After sixteen years, I decided to consolidate some of my old pensions including this one. I checked that I would not lose any benefits or incur any costs by moving it (I wouldn’t) and then asked for it to be transferred to Hargreaves Lansdown where I had been consolidating my finances. The £5,000 that I had personally paid towards my pension (plus £10,000 from employer and any government contributions), was now worth a rather impressive £101,000. That was from nine years of pension contributions between my late 20s and my late 30s. Over my working life I did contribute to a number of other pension schemes, but this one is worth highlighting as it clearly demonstrates a fundamental principle of pension contributions. It doesn’t matter if your contributions are not that great to start off with. Contribute what you can, it will be supplemented by your employer and the government. But more importantly, starting early gives you the gift of time, and time in the market is what will help your pension pot grow. There is also another investment that we should look at briefly, and this one should also be considered for early and regular investment if you want to retire before your official government retirement age. This is the stocks and shares individual savings account, more commonly referred to as the stocks and shares ISA. When I was in my 20s ISAs didn’t exist, however, there was something that was very similar which was a Personal Equity Plan, or PEP for short. These were eventually superseded and by 2008, these PEPs had all been converted to stocks and shares ISAs. Anyhow, I started my PEP while in my 20s and continued to invest small amounts over the years. Currently an ISA has an annual contribution limit of £20,000 and so this is very generous. I will stress, this is the maximum you can put in each year, but you don’t have to invest as much as that. As with a pension, any small, regular contribution from an early age will grow with time, and it’s the development of a habit to invest that is as important as the amount invested. As you get older, and earn more money, you can increase your monthly contributions as appropriate. You may be wondering why bother with a stocks and shares ISA if you already invest in a pension. Whilst the underlying investments are often similar, the tax treatment of a pension and an ISA are different, and having both can give you more flexibility when you retire. As an example, the current personal tax free allowance is £12,570, and so you can withdraw this amount each year from your pension without paying any tax. In other words, if you take much more than £1,000 per month from your pension, you are going to have to start paying tax on it. However, with an ISA, any money you withdraw is tax free. So if you have money invested in both a pension and an ISA, once you retire you can minimise the amount of tax you pay by utilising your investments in both. As an example, you could take £1,000 per month of tax free cash from your pension and another £1,000 per month, tax free, from your ISA, giving you a potential retirement income of £2,000 per month completely tax free. Another reason to utilise an ISA alongside a pension is that you cannot access your pension money until you are 55 years old (but expected to rise to 57 by 2028). Therefore, if you need income before this, you definitely need to invest in an ISA to enable you to retire when you want. Many people dream of retiring early but never achieve it. However, it is possible to retire early if you make the right plans and start investing as soon as you can. Time is the friend of the investor, as while in the short term your investments can go down as well as up, over the long term, with a diversified portfolio of quality investments, your pension and ISA should both grow to allow you to retire by the age of 55. However, contrary what anyone might say, there isn’t just one approach to achieving an early retirement, and the options I present here are just that, options. This isn’t financial advice, but reflections from my own plans to retire early. Did I do everything right? Probably not. Did I manage to retire at 55? Yes, I most certainly did.  Guest blog written by Jordan from Sterling with Sterling Pleasingly, it is slowly but surely becoming more and more 'trendy' for the average Briton to start looking deeper into their personal finances. For many years we have set our money to autopilot and allowed it to go in and out of our bank accounts without utilising it in a way that grows our net worth. In fact, I would argue that most people in the UK couldn't tell you what their net worth is, can you? Do you know your projected retirement age? These are questions we aren't taught the answers to at school but perhaps ones that are vital to get your head around if you are to retire early. So, without further ado, here are the 5 rules I swear to live by in order to retire early.

Take home pay - know your monthly income figure Before spending money, you must know your ‘starting point’. Once you are paid, see what you have. Then, work out what your necessity spends are until you next receive income. Now, with just a few minutes sitting down looking at your finances, you know how much you’re starting with, what you have to spend and what you can spend; this is the value of knowing your take home pay. It’s the foundation on which you will build your future. Remember, if you are to retire early, the difference between what you start with and what you have to spend is best off being invested or saved. The gap between income and expenses is the one thing that will allow you to reach your financial goals. Conveniently, this leads me onto my next rule… Pay yourself first This rule refers to what I call ‘me money’. This, as explained with the first rule, is the difference between my income and my spend. The bigger this gap, the sooner I can retire. I’m sure that anybody who has retired early will tell you that this ‘me money’ needs to be utilised before you spend money on life’s necessities (bills and groceries etc). Pay yourself first or else you won’t pay yourself at all. Set yourself a budget - without a budget the spending never stops Once again, this next rule ties in with the previous one. If you fail to start the month with a budget in place, then how can you track your spending? What are you tracking it against? Chances are, without a budget or plan in place, you will spend more money than necessary in all areas. Whether it be transport and petrol/diesel, groceries and essentials, or even leisure and hobbies… without a budget, your spending will spin out of control. Work out what you currently spend on each ‘category’, then work out what you want to spend on each category – try and find a reasonable limit using these two figures. If you can keep to these limits each month whilst continuing to grow your income, then the amount of ‘me money’ you have each money will only increase. Make sure not to live above your means! Don't borrow what you can't repay This rule is simple. It shouldn’t really require a lot of explanation. These days there are multiple credit options on offer to the British public. Often, you will be approved for these flexible credit options despite having a poor credit score. This can be tempting and can promise to pull you out of a sticky financial situation, but this is not always the reality. If you can’t afford something right now, and intend to use credit, then ask yourself what will be different in the future? What will be different in 6 months from now that means you will be able to pay off the debt? If you aren’t certain that you will be able to pay off the debt, then don’t borrow that money! Think before you buy - will future you regret this purchase? This is self-explanatory. Try to avoid buying things that you will regret buying a few months down the line. Of course, this is easier said than done. So, I pass down a rule of thumb I was told a while back… open the notes app in your phone or if you’re old school, get out a notepad and pen. Now, write down that thing you really want to buy, that thing which (right now) you’re sure you can’t live without. Okay, now, the hard bit… don’t buy it. Allow 3 months to pass. Do you still want it? Have you even remembered that you wanted it in the first place? Do you even know where that notepad and pen is? If the answer to these questions is no, then you would have saved yourself some money. Money that would have been spent on something which you wouldn’t use, something that would only depreciate in value. Instead, you will now have some more ‘me money’ which can be invested in your future! And by the way, if the answer to those questions was yes and you do still desperately want to make that purchase then good for you! You’re all set and ready to buy something you actually need and desire. I can only hope that these rules stick with you and that you implement them in your life. I truly believe that in the world of personal finance, these are rules to live by. They are principles. Foundations of a financial philosophy. When it comes to planning for your financial future, now is always the best time to start... For more insight regarding all things personal finance visit sterlingwithsterling.com and have a read of our blogs! Until next time, Jordan Looking on social media you could be forgiven for thinking that the only sensible way to invest is through an index fund. So many ‘finance gurus’ espouse the simplicity and low cost of just buying into a fund that tracks an index, often the S&P Index, that surely anything else would just be plain silly? For those of you that don’t know, an index fund is a fund that is constructed to match or track the components of a specific financial market. So rather than trying to beat the market, the fund just rides along on its wave. Many studies have shown that this approach can often do as well, if not better, than paying lots of clever financial types to construct an actively managed fund of specifically selected companies, that they believe will perform better than average. The S&P 500 is just one index that a fund can follow. The S&P 500’s full name is the Standard & Poor’s 500 index, which is an index of the top 500 companies in the United States and includes such behemoths as Apple, Amazon, Alphabet (Google) and Meta (Facebook). With big brand names like this you would expect this index to do well, and it does! Although S&P 500 index funds seem to dominate social media discussion, I guess because these top 500 US companies dominate the world stock markets, there are thousands of other index funds tracking all sorts of different markets. So if you want to track the world market or the UK market, for example, you can do this as well. So let’s just look at the S&P 500 briefly again. In recent years it has done very well in comparison to other markets, growing on average at around 10% each year over the last ten years. So this does look like a sensible investment option, surely?  The S&P 500 Well yes, it probably is. And whilst you can look at past data to give you an idea of what might happen in the future, in reality, without a time machine, we don’t know for sure what will happen in the next couple of years, let alone the next ten. What do all the finance sites say? ‘Past performance is no guarantee of future performance’, or words to that effect. They say this for a reason; things change, trends come and go, and markets can ‘wobble’.

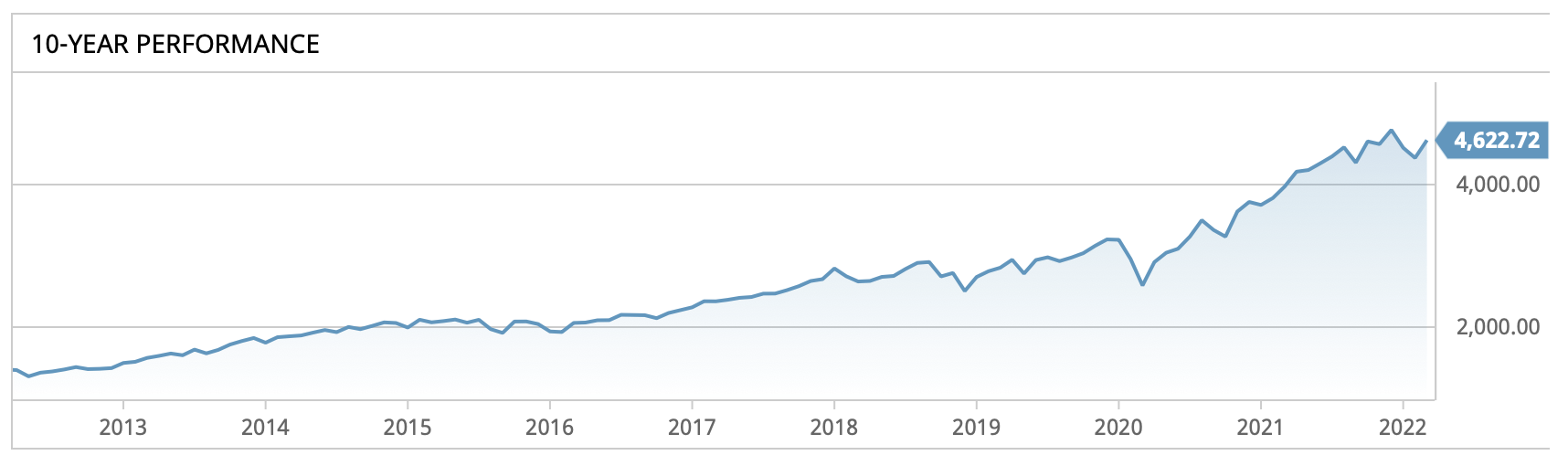

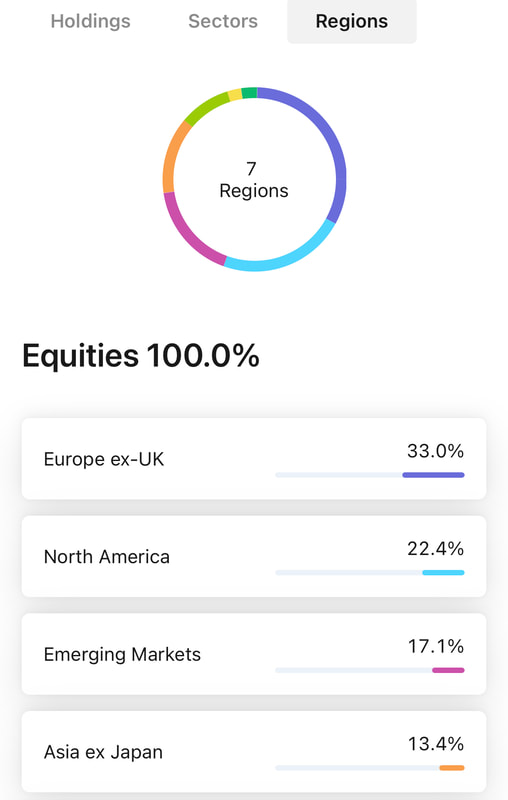

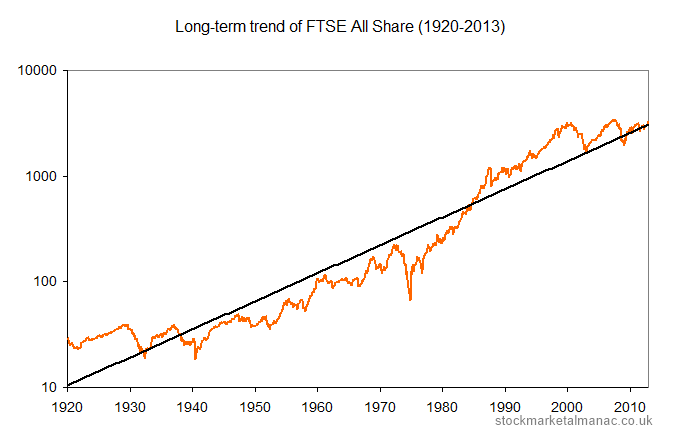

And this is why, when I invest, I include plenty of diversification in my investments. And when I say ‘diversification’, I’m not just talking about different countries, but also different asset types as well. Because when some of you portfolio is taking a dip, a well diversified portfolio will have another asset type or another geographical area riding high. So index funds; yes they can be great, but if you are going to invest in them, make sure you diversify across asset types and geography when selecting them. Piling all you money into one index fund isn’t necessarily the best strategy. So why don’t I routinely invest in index funds? I believe that when investing you should be clear on your overall objective. If your objective is to grow overall value of your investment over the long term, then an index fund is a reasonable investment option to take. If you want a simple way to grow your portfolio with minimal input, then a group of diversified index funds may just be the thing for you. Set up a monthly direct debit to keep topping them up and watch your portfolio grow over the years. Forget about them, get on with your life and just do a check and rebalance every year or so. But what if you have a different objective? Like I do. I have given up my ‘normal’ day job. I retired, for want of a better term, about 3 years ago now and have since been living off income from my investments. To do this, I moved my investments from index funds into a number of actively managed funds, which do have slightly higher charges. However, on the plus side, these are giving me a regular income in the form of dividends and interest. I currently get just over 4% in ‘natural yield’ on these investments. That is to say, the dividends and interest alone are giving me £4,000 per year (around £350 per month) for every £100,000 I have invested. I can withdraw this as income without touching the original capital. Currently I can manage on less than the yield I’m getting and so some of the excess is being reinvested, as I’m sure I will get some years where the investments won't perform as well. This so called ‘Natural Yield’ approach does mean that you can never be certain of the amount of money you will ‘earn’ each year, but with a bit of planning and monitoring, your investments could provide an income for the rest of your life. As part of my strategy to diversify I have also put money into a number of other investments outside of the traditional equities and bond markets. There are a growing number of opportunities springing up, some of which may be higher risk, but some which actually may be slightly lower risk than many equity markets. The higher risk investment that I have invested some money in to is crypto currency. This is a very volatile market and not for the feint hearted. However, if you are brave enough, then there could be some significant long term gains here. I only invest small amounts here and that is as much through intrigue than anything else. As my confidence grows with time, I may invest a bit more. A slightly less risky option that gives me 5% is through an easy access account called Sterling Boost that Ziglu have recently launched. This is quite a new and innovative product where they converting your money to a stable-coin which is then lent out and you earn a portion of the interest that they get. Stable-coins are less volatile than other cryptocurrencies as they are linked directly to something of known value such as the US dollar, but still have all the advantages of crypto currencies by running on the blockchain. There are also a number of property based companies that I have investments with. These are essentially crowd funded property investments, either buying a part ownership in a property and receiving rental income or by supporting property developers through peer to peer lending. If you want to find out more about these then check out Proptee where you can buy fractions of properties through the magic of NFTs and Kuflink, where you can support property developers by lending money that is fully secured against the property being developed. These types of investments can pay out in the region of 6% -10% and so compare well to more traditional equity market investments. However, these are newer investments and so only time will tell if they were a worthwhile investment or not. Now where did I put that time-machine?  Interest rates on savings are very low at the moment and inflation is rising. So any money in traditional savings accounts is actually losing money in real terms. Money invested in the stock market however, can actually beat inflation and give you a positive return. So why do so few people invest? One reason is possibly that it is seen as complex, expensive and only for the rich; with large sums involved and expensive trading fees through stock brokers. But that isn’t the case anymore as with the rise of modern technology it is now easier to invest than ever before. If you have a smartphone and £100 you can start investing now. Let’s look at two examples. The first is Freetrade. As it’s name implies there are no trading fees through Freetrade. On its basic plan there are no costs whatsoever. They do have other plans that you can move to with a small cost that give you additional benefits. But as a new investor, the basic plan is sufficient. Freetrade allow you to purchase shares and ETFs (exchange traded funds), which are essentially a ‘basket’ of shares with a common theme. This is all done through an app on your phone and it’s all pretty intuitive. I have been using Freetrade for over a year now and it works really well. As you can see below, the return over the last year has easily exceeded a traditional savings account (although there has been more growth than usual following a drop in the market at the beginning of the covid pandemic).  If you do decide to sign up to Freetrade you can get a free share worth between £3 and £200 if you use my link below. For transparency I will also get a free share worth between £3 and £200. Check out Freetrade The second investment platform I want to look at is Invest Engine. This one is slightly newer than Freetrade and works slightly differently. Nonetheless it also is very easy to use. Invest Engine don’t currently have any individual company shares to invest in but instead focus on ETFs. They have a select range of around 350 ETFs covering a range of markets and you can either self select which ones you want to invest in or for a small fee (0.25%) they will select for you and monitor/adjust as necessary. Because Invest Engine are currently growing their customer base, they have an attractive offer for new investors. When you open an account they give you £50 to invest. This gives you a no risk opportunity to learn how the platform works. Once you are happy you can then invest £100 of your own money and if you keep this on the platform for a minimum of one year you get to keep the original £50. On top of this, if you use my link below you will get an additional £25 referral bonus. So for a £100 investment you get £175 without any market movement added in! A new feature just added to Invest Engine is the ‘Analytics’ tab. Here you can see how your money is invested across sectors and regions as well as individual companies. I really like this new feature which really helps you 'diversify' your investments around the world and across different sectors.   ‘Less than 5% of Brits currently have a stocks and shares ISA’ according to Finder (https://www.finder.com/uk/stocks-and-shares-isa-statistics) And of those that have stocks and shares ISAs, the average amount invested is £9,331. This is despite the fact that the annual allowance for investing in a stocks and shares ISA is £20,000 and that any income or gains received is completely tax free. If you don’t feel that these statistics are shocking, then you should. Why is it that the people of the UK are not taking advantage of the benefits of these stocks and shares ISAs, when historically the amount you can grow your investment through such an ISA is so much better than leaving all your money in a traditional savings account earning minimal interest. I believe that one of the reasons that people shy away from stocks and shares in general is the ubiquitous warning you see with all of these types of products: “All investing should be regarded as long term. The value of investments can fall as well as rise, and you may get back less than you invested. Past performance is no guarantee of future results. Your capital is at risk” For many, this statement is a real turn-off for investing. Why would anyone want to put their money into something where the value could fall and they risk losing all their money? No thanks, I’ll put my money in the bank where it is safe. But let us look at the reality for a moment. Below is a graph of the last 100 years of the FTSE All Shares Index.  You see similar patterns in most other markets across the world. The trend is clearly one of continued growth, and usually at a rate which is significantly better than you can achieve in your bank’s standard savings account.

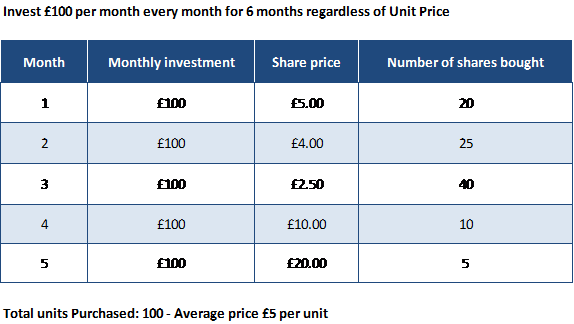

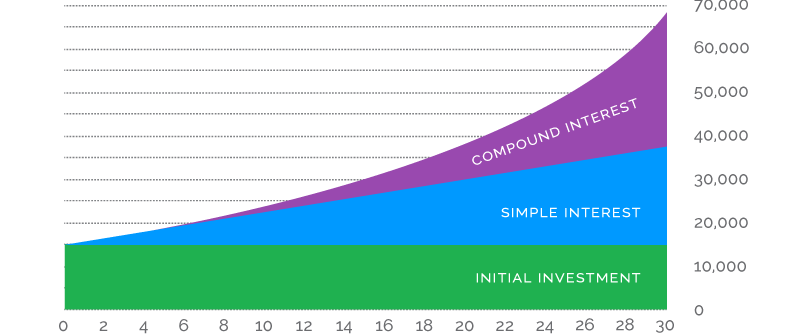

From the above graph you can see that there are some years that show a drop in value; and this is what the standard warning is all about. If you invest when the market is high and then withdraw within a short time frame where the market has temporarily dipped, then you will lose money. Investing therefore is about the ‘long game’. Money invested should stay invested. Leave it there and let it do it’s work, earning money for you. Apart from ‘time’, there are other ways to minimise the risk of a loss. The key way of minimising the risk is through diversification. By diversification we mean, invest in a number of different markets. If one market dips, then another market may be growing and offset this. You can also diversify through a number of different types of assets; company shares, corporate bonds etc. Many people might see this as added complexity that will put them off investing. But there are companies/apps that can help you with this, giving guidance or even having complete diversified portfolios already for you to invest in. One example is the app based investment broker, InvestEngine that for a small fee will put together a range of funds for you and manage them on an ongoing basis. However, one of the best things you can do, is to carry out a little bit of research yourself so that you can become confident at selecting a range of funds to invest in, through a broker such as Hargreaves Lansdown or Freetrade, where you have complete control over where you invest.  In order to retire early you need to become ’financially independent”. This means that you need to be able to live your life without the need to ‘earn a living’ through traditional employment. To achieve this there a few clear steps to take and a few key principles to understand. In this article I want to cover some of these steps and key principles as initial ‘food for thought’ for someone who is looking to achieve financial freedom. Even clever people are stupid when it comes to moneyIn schools we generally are not taught about finances. You may pick up a bit from parents, but then they haven’t been taught either and so bad habits and false assumptions are passed on and the lack of understanding is perpetuated from generation to generation. Maybe the truly wealthy are immune to this as they pay an army of accountants to help them look after their money. But for most people, this isn’t an option and if we want to understand money we need to look elsewhere. In the end it is down to all of us as individuals to learn about finances and increase our own ‘Financial Intelligence’. The fact that you are reading this means that you are probably ahead of most people. This article isn’t going to cover everything though. It’s not even going to cover ‘a lot’! It will only skim over a few principles as a starting point. If you really want to improve your Financial Intelligence you will have to do a lot more research, and check out some reliable sources to ensure that what you learn is balanced and accurate. Don't fall in to the 'Debt Trap'!We seem to accept debt as ‘normal’ these days. People talk about how great their credit score is and how much credit they can get on their credit cards as if it’s something to aspire to. But is spending beyond your means really a great way to become financially independent? Or does this just generate the illusion of wealth? Buying ‘stuff’ on credit usually means you are paying interest on top of whatever you have bought, and the interest you end up paying can be quite considerable. If you have high interest debt then this is particularly true. Expensive credit card debt or car loans at a higher interest rate than you can achieve through passive income (see later) will mean that you are taking one step forward and two steps back. One exception to this could be a mortgage debt, if it is at a rate of below 4%. This is because the money you owe through your mortgage might be better utilised as an investment earning a rate above 4%. However, this isn’t clear cut, as paying off a mortgage can be a great weight lifted. The monthly repayments are usually one of your largest regular monthly outgoings, and reducing this can in itself be a great step towards ‘financial independence’.  'You can’t have money, and spend it'Whilst some people in well paying jobs seem to have a lot of money, many of them don’t as they also spend a lot of money. As I was told as a boy, ‘You can’t have money, and spend it’. They may be earning a lot, but they probably have little invested and live from payday to payday in the same way that many others do. They may believe that their primary residence, their home, is where their money is invested, and to some extent this is true. However, to release that money, they need to first sell their home, which isn’t always easy and never guaranteed to turn a profit. A key step to Financial Independence is to start thinking about where your money is spent. Call it a budget, a financial plan or whatever. But you need to start looking. It could just be a sheet of paper with a list of everything you have spent money on over the last 12 months. It's all there, in your bank and credit card statements - get them out, and make a list. Then look what can be cut and where you can save some money. You need to free up some spare money in order to be able to invest. The rich buy assets, the poor buy liabilitiesDid you know, that rich people don’t actually work for money? Rich people get money working for them. This is where it’s important to know the difference between an asset and a liability. There are plenty of complex definitions for these that you can look up on the internet. But in a nutshell, an asset is something that will generate money and a liability is something that will lose money. If you want to become financially independent then you need to focus on buying assets and not liabilities. Use the money you freed up when you did your budget to buy and hold assets. Keep buying them, month in month out. Remember to always ‘pay yourself first’. By this I mean you should be investing this money first before dealing with your other bills. Think about setting up a direct debit each month so that it happens automatically. This is how you get your money working for you. Your assets will produce passive income (you don’t have to work to earn it), and as your assets grow, so does the amount of passive income you earn. Every pound you invest in assets is a pound working for you. Leave it alone and it will continue working for you. Don’t focus so much on how much you are earning from your day to day job. Focus instead on how large your asset portfolio is and how much it is growing. This is your own ‘business’ and you need to look after it first and foremost. So what assets should you be buying? Well, that is up to you. One of the easiest assets to buy these days are funds that invest in shares and bonds on the stock market. This can be done through online brokers such as Freetrade* or Hargreaves Lansdown (other brokers are available).  Pound Cost AveragingYou may be aware that the stock market goes up and down and so you often see the phrase that investments may go down and you may not get back as much as you put in. This is something that I believe puts some people off investing. However, historically this has only ever been true when investing for the short term. If you truly believe that owning income producing assets is the path to financial freedom, then why would you sell them? You are in for the long term and when you look at longer term trends, the stock market has done very well. One way to also help with the ups and downs of the stock market is through ‘pound cost averaging’ - by investing on a regular basis, such as monthly, you will buy more when the cost is low and less when the cost is high. This smooths out some of the ups and downs in the market and means that overall you are buying at an ‘average’ cost. Small and often is the way to go!  Failing to plan is planning to failWhen you do start to buy assets, don’t just invest based purely on the opinions of others. If you do, you will be pulled all over the place as different people will give conflicting advice based on what they believe your priorities should be. Be clear on what you want to own and why. As an example, my assets generally produce an income in the form of interest or a company dividend. For me that is important as I want a regular income now. If you are currently in employment, and don’t yet need to receive a regular income from your assets, then a different set of assets may be more appropriate, such as high growth accumulation funds (accumulation funds automatically reinvest any earnings back into the fund which results in compound interest). You can always then switch these when your objectives change and you want to start releasing the income. So, have a plan, know why you are investing, what your objectives are, both in the short and long term, and be clear on what you want to invest in. ‘Compound Interest is the eighth wonder of the world. He who understands it earns it, he who doesn’t, pays it’ (Albert Einstein)Most people are familiar with the concept of earning interest. You put money in the bank and they pay you a bit of interest each month. It’s usually pitifully low and doesn’t keep up with inflation and so in reality you are losing money. But that’s another story! Well, compound interest is where any interest you earn is paid back into your ‘savings’ and so the following month you not only earn interest on your original sum, but you also earn interest on the previous months interest. In the short term, this isn’t that significant. However, in the long term, this compounding really makes a huge difference. This means that the money you invest in your 20s and 30s is so much more important than money you invest in your 40s and 50s. Small amounts invested when you are young become surprisingly large when you are older. Compound interest and time are very important concepts for long term investing. In the graph below you can clearly see that compounding the interest over 30 years has nearly doubled the value of the investment compared to just simple interest.  Prepare for the WorstTo make sure that your plans stay on track you should always have a contingency plan. Occasionally things go wrong. Your car unexpectedly breaks down, or you lose your job. Being prepared for these events mean that your plans are not thrown into disarray! One way to do this is to have an emergency cash fund. Many people suggest 3 to 6 months of living expenses is the right amount (unless you are retired in which case 1 to 3 years is recommended). But really, again, it is up to you how much you have in your emergency fund. Some of this should be in easy access accounts so that you can use it immediately if needed. But you could have some saved in fixed term accounts to give you a bit more interest (as easy access accounts pay very poor interest rates). One of the tricks that I employ is to ‘ladder’ my savings. As an example, say your emergency fund is £10,000. You could keep £4000 in an easy access account which is likely to be enough for most emergencies that require immediate funds. You could then save the rest in a series of 1 year fixed rate savings accounts, say £500 each month. Then after 12 months, your first fixed rate account matures and £500 is released. This can then be put back into another 12 month fixed rate account if not needed or used as part of your contingency plans if necessary. Each month another £500 is released and so on. Diversify your AssetsDifferent assets will do well at different times. It therefore makes a lot of sense to hold a variety of different assets. If one asset is performing poorly in a particular year, another one will compensate by doing better. Diversification should be on both asset types and geography. So if you are invested in the stock market, you can have assets that hold equities (company shares) and assets that hold bonds (company IOUs). Both of these are also available across the world, and so when the U.S. is doing well, Europe might be going through a slump. There are thousands of different assets available and only you can decide which ones are right for you. But once you have a plan and know what you want to buy, make sure you have enough diversification so that any dips in the value of your assets are smoothed out. So, in summary….Spend the time you need to learn about finances so that you can make the right financial decisions. Pay off your debt and make a budget/financial plan so that you know where you are spending your money and where you can make savings. Buy assets on a regular basis that will provide income over the long term. Minimise risk through diversification and keep an emergency fund in easily accessible cash. At some point, your income producing assets will provide you with enough income that you no longer need to worry about working for someone else. You are now Financially Independent!

Granola RecipeThis recipe for granola isn't going to save you money, or make you healthy. However, it does taste good.

Mix everything together, except cranberries, and spread evenly on 2 large baking trays and put in oven for 13 mins on 160*C. Allow to cool and then add the cranberries.  Peer to peer investments are an alternative form of investment that have grown over the last few years and are now becoming more mainstream. Essentially they work as a 'crowd sourced' loan for people who want to borrow money. This is usually organised through a 'Platform' which matches people who want to borrow to those that want to invest. Some of these 'platforms' are now so well structured it feels more like depositing money in a bank. However, it isn't the same as depositing money in a bank (which usually has FCA protection up to £85,000), as with peer to peer lending there is no protection - it is NOT saving, it's investing, and there is little protection if things go wrong. Having said that, many people feel that peer to peer investing is less risky than investing in shares, and it can pay more in interest than traditional savings. As always, a key way to mitigate any risk is to diversify. Therefore, peer to peer shouldn't really be seen as an alternative to other investment strategies, but as a compliment to them. So a fully diversified investment portfolio should include shares, bonds and property as well as peer to peer investments. You should also keep some money aside as cash in an easy access account that can be accessed in difficult times (think 2020 and pandemic!). There are a number of peer to peer platforms that you can look at for investing, which allow you to lend to different types of borrowers and diversify across both platform and borrower types. Below I have ranked the four peer to peer platforms where I have the most experience and have highlighted some of the key points about each. Currently only Kuflink is open to new investments. However, this is my number one choice and would be a great place to start if you want to explore peer to peer. 1. KuflinkKuflink are a peer to peer company that focuses solely on lending to property developers. This in itself makes them slightly different to many other, more generalist P2P companies, but what I also like is that they also invest up to 5% of their own money into each development loan alongside the crowd sourced money. For me, this gives me greater confidence that they are truly looking at lending responsibly. In addition, the money lent is secured against the property being developed and usually with a realistic LTV (loan to value - i.e. the loan given is less than could be raised if the developer collapsed and the property had to be sold to recover the loan amount). Whilst the Kuflink platform was built in 2017, the company behind Kuflink have been providing bridging loans since 2011 and they have won numerous awards within the industry. Once signed up to Kuflink, you can choose to let them select the investments for you (auto-invest), or you can select yourself which properties to invest in (select-invest). Within the auto-invest option you can also invest within an ISA wrapper and there is also a SIPP (self invested personal pension) option. I personally invest using the select-invest option as that enables me to choose which property developments I invest in and how much I want to invest in each. I feel this helps me keep control of ensuring a good diversification across properties and it also gives me the option to take my interest monthly which fits in nicely with my passive income strategy. During 2020, Kuflink have continued to lend to property developers and continued to pay interest to developers. In this respect, Kuflink seem to have weathered the pandemic better than most and so my faith in them as a business has remained high. Currently I am earning around 6.8% interest each month, but this can be boosted to just over 7% if you opt for annual payments rather than monthly. This level of interest, along with loans secured against property and the ability to diversify across many property developments across the UK has made me position Kuflink as my number 1 peer to peer platform for 2020. If you decide to invest in Kuflink, by using my referral link you could receive up to £4,000 cash-back: -> go to Kuflink 2. Lending WorksLending Works is a very simple and easy to use peer to peer offering which lends to individuals with unsecured loans of up to 5 years. Diversification is built in as your investment is split across a number of different loans. In addition, Lending Works has a 'Lending Works Shield' which provides 'first-loss cover' across all of it's loans. This 'Shield' is funded by the borrowers as part of the interest they pay on their loans. Then if anyone does default on their payments, this shield can be used to cover the due payments to lenders. Lending Works advertise the fact that no lender has to date lost any capital. Apart from the simplicity and easy to use website, another great feature of Lending Works is that you can set your capital to be re-lent and any interest to be paid out. This means that you can keep your money invested and earn a regular monthly passive income through Lending Works. Lending Works advertise interest rates of up to 5.4% from lent money which can be held within either a general account or within an ISA wrapper. However, during 2020, Lending Works have found the pandemic a challenge. They stopped lending money out earlier this year which has meant that repaid capital has accrued within accounts. This money has been available for withdrawal and no money has been lost (so far). It does mean though, that overall interest for the year has fallen below advertised rates and is currently closer to 3% rather than the pre-pandemic 5.4%. They plan to start re-lending to borrowers in January 2021. Lending Works have recently had an investment company invest heavily in them and their platform. This can only be good news for Lending Works as a company and I believe that as we move out of the pandemic, and we start to get back to normal, they will remain a good option for passive income generation. If you decide to invest in Lending Works (once the freeze on new investments is lifted in January), by using my referral link you could receive £50 cash-back: -> go to Lending Works 3. Funding CircleFunding Circle lends to small businesses which is different to the other P2P lenders listed here. Money invested in Funding Circle therefore increases your diversification as you lend to a different type of borrower. Also, to help with diversification, Funding Circle split your investment across a number of different businesses. For example, if you invest £2,000 they will split that across 20 small businesses so that you end up lending no more than £10 to any individual business. The interest rate that they advertise you can expect includes any expected defaults. So unlike Lending Works, there is no 'shield'. Losses are expected and built in to their model. Funding Circle advertise an interest rate range of 4.5% to 6.5%. My investment is currently returning around 5.9% which I believe is reasonable especially considering the difficult year we have just had. Funding Circle is another P2P lender that is currently not lending investors money out to borrowers. This is because at the moment they are involved with the government CBILS (coronavirus business interruption loan scheme) lending programme and this isn't something that can be invested in through individual (retail) investors. This means that any repaid capital coming in to your account isn't re-lent and so this can be withdrawn on a regular basis if you want. If you want to invest via Funding Circle once they start accepting new retail/personal investments then you can find them here -> go to Funding Circle 4. ZopaZopa advertises itself as the 'World's First P2P Platform' and highlight that they have been in business now for 15 years. If nothing else, this should give you a certain amount of confidence about how they run this type of business. Not only have they weathered the 2020 pandemic, they also weathered the 2008/2009 financial crisis. Zopa lend to individuals in the same way as Lending Works do. They don't however have a 'shield' to protect investors but build in defaults to the advertised rates that you can earn. In reality, this means that the rates you can earn through Zopa are lower than many other P2P lenders and currently advertised as between 2% and 5.3%.

Recently, Zopa have also launched as a bank with one of their first offerings a credit card. How their bank offering will affect their P2P business isn't really yet known, but currently they are saying that they will be run as two separate businesses side by side. Zopa have continued to lend during 2020, but have been more careful to whom they lend to and thus waiting times for any investment to be lent out are now running to over a month. This is quite a long time for your money to not be earning anything, sitting in a queue, waiting to be lent out. As we move into 2021 and the pandemic becomes history, then this situation is likely to change. If you want to invest with a company that has been around the longest and weathered two financial crises, then Zopa may be a good starting point for you. If you want to invest with Zopa, use the following link -> go to Zopa

A lot of companies these days will provide you with a mobile phone, as part of the tech you need to effectively do your job. Having a mobile phone will allow you to keep in contact with colleagues and customers alike, through calls, texts, messaging apps and email. However, when you finish work for the day, or for the week, do you then turn off your work phone? Or do you, like many, keep it on so that family and friends can contact you outside of work hours? Having a work phone that you can use for both work and private can save you a fair bit of money as you don't need to buy your own phone and don't need to pay for your own contract. On the face of it, this seems like a real 'win', a free phone to be used as much as you like!

But now ask yourself the following questions; how often do you look at work emails outside of working hours? How often does a work colleague or customer call you when you are spending 'quality time' with the family? Is this really the best way to create a great 'work/life' balance? Do you find that it's sometimes difficult to 'switch off' and 'unwind'? There IS an alternative - get a second mobile phone for personal use. This doesn't have to cost you a lot as it doesn't have to be the newest all singing and dancing phone - just something that you have with you evenings, weekends and when on annual leave, so family and friends can contact you when your work phone is switched off and locked away. You can even buy a refurbished phone if you want, for example through Giffgaff, and then use a Pay As You Go (PAYG) sim - often much cheaper than getting a contract. Giffgaff also sell monthly bundles which they call 'Goodybags" starting from as little as £6 per month with unlimited calls and texts. It's a bit like a 1 month contract, but you can start and stop whenever you want. You can manage and monitor your usage via the handy Giffgaff mobile app and there is a great online community who can answer your questions quickly. And if you get a Giffgaff phone sim by clicking on the following link you will even get a £5 'thank you' as a bonus!

|

RSS Feed

RSS Feed